It’s the weekend, but our fresh Financial Crisis does not sleep. And a recent study says we’ve only seen the tip of the iceberg.

The Washington Post yesterday wrote: “If banks were suddenly forced to liquidate their bond and loan portfolios, the losses would erase up to 91 percent of their combined capital cushion.” In other words, we were already right up against the edge.

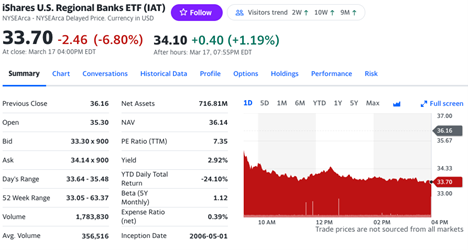

The Post cites two studies that total unrealized losses in the system are between $1.7 trillion and $2 trillion. Total capital buffer in the US banking system: $2.2 trillion. That’s about a 10 percent to 20 percent buffer. And now running into a market crisis where bank stocks have declined by about a third in the past few weeks, and are now at a P/E ratio of 7.35.

Meanwhile, the Wall Street Journal last week wrote about a brand new study from Stanford and Columbia finding 186 banks are in distress — possibly to the point of seeking a bailout. The study estimates that hundreds of banks are in worse shape than SVB: hundreds have larger losses than Silicon Valley Bank, and hundreds have lower capitalization buffers in case of distress than Silicon Valley Bank.

How did it Happen?

In short, while tech bros and loose bankers hog the headlines, what drives hundreds of banks to the edge is our crony banking system.

In this case, rapid Fed rate hikes crashed into a banking system that fractional reserve banking and the Fed’s “Lender of Last Resort” (LOLR) permanent bailout have driven to permanently drive as fast as possible, as close to the edge of the cliff as possible.

Together, the moral hazard has given a green light to those reckless tech bros, to those loose bankers who hand out millions — it turns out hundreds of billions. And it drives the entire banking industry to use opaque accounting tricks to hustle sleepy regulators and innocent taxpayers and dollar-holders who get stuck with the bill. The bankers themselves sleep like babies because they know you’ll cover their losses, but they keep their wins.

What turned this rigged casino into a crisis is in the past year the Fed hiked rates at the fastest pace in 50 years, from 0 percent last March to 4.5 percent to 4.75 percent today. They did this in a desperate bid to cancel the inflation they caused by financing $7 trillion in deficit spending and Covid lockdowns. Indeed, those of us who wondered why voters stood by meekly had only to look at the flood of money going out the door.

These reckless hikes savaged long bond prices, by far the most popular asset in bank vaults: Across the board, long bonds fell 20 percent, feeding an estimated 10 percent plunge in all bank asset values. In essence, the bank thought it had a dollar in the vault, but turns out it only had 90 or 80 cents. In the case of high-flyers like Silicon Valley and potentially hundreds more, it was more like 60 cents. Few banks can survive that.

What’s Next

This slow-motion train-crash is now making contact: Last week $152 billion in loans went out the Fed’s discount window — the discount window is where desperate banks go when nobody else will lend, like a junkie selling the TV.

That dwarfs even the worst of the 2008 crisis at $111 billion. Keep in mind back then was months into the alleged financial crisis of the century. Here we passed it at week one.

What’s next? Probably a lot of pain and a lot of inflation. We the People will survive — after all, the real assets don’t vanish: the food, cars, and electricity are all there. It’s a paper crisis, but unfortunately that paper crisis has sucked real Americans in, suckered them into putting their life savings into the care of a bunch of degenerate gamblers in expensive suits. And it can bring enormous collateral damage to the wider economy that, yes, provides that food, cars, and electricity if government steps in, as it usually does.

Concretely, I’d expect trillions of dollars in bailouts, driving inflation back towards last year’s highs, perhaps even into double digits. This while the economy careens into recession, indeed into stagflation. The Fed will abandon the inflation fight it started, opting instead to bailout the bankers who it serves. And We the People, as always, will pay the tab: for the bailouts, for the inflation, for the stagflationary crisis that’s looking increasingly likely.

How to protect yourself? If we’re headed for a crash, you want hard assets — Bitcoin if you understand it enough to hold in a storm, gold if you don’t. Periods of chaos drive big swings in markets and prices, so you’ll be tempted along the way into equities and bonds. But going by the principle that the first goal of investing is being able to sleep at night, I’d probably keep the powder dry until the smoke clears.

What do you guys think — how will this pan out? Does it get to the cat food stage or just down-budgeting from Beyond Meat to dog food? And let me know what you’d like to hear in future posts and future videos.

See you next time!

This article first appeared on Peter’s Substack page.